Memo

To: Interested Parties

From: The Bresnahan Soaring Costs Campaign

Date: February 6, 2026

Subject: Congressman Rob Bresnahan Must Act To Reverse His Health Care Price Hikes

Talk is cheap. Health insurance is not. Congressman Rob Bresnahan voted for historic and devastating cuts to Medicaid – to pay for tax breaks for billionaires. Then, he failed to act in time to prevent higher premiums for millions of working families who are struggling to afford health insurance.

Open Enrollment has ended in Pennsylvania. And while Congressman Bresnahan sold stock related to his historic health care cuts, Pennsylvanians are already paying sky-high premiums or opting out of coverage altogether. According to Pennie, there’s been a 22% decrease in new enrollees since the start of Open Enrollment.

Now, Congressman Bresnahan must act to reverse this health care crisis that he helped to create. Congressman Bresnahan helped Congressional Republicans keep the government shut down last fall rather than working to extend the ACA tax credits before it was too late to stop Americans from seeing health insurance price spikes. He finally voted for tax credits in January, only after the tax credits had already expired.

Despite his bowing to sustained pressure from his constituents and the Bresnahan Soaring Costs Campaign and ultimately voting to extend the tax credits, his last minute support was absolutely too late to avoid raising health insurance costs for consumers.

Georgetown Center on Health Insurance Reforms on October 15:

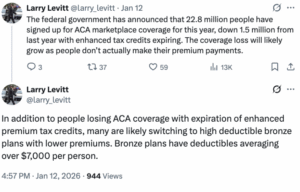

Indeed, Congress has already waited too long. Even if the enhancements were to be extended tomorrow, millions of people now inevitably face higher premiums for the year, because insurance companies have finalized their rates assuming that smaller PTCs [health care tax credits] will push healthy people out…If an extension passes at year’s end, coverage losses will be 1.5 million due to the delays alone, according to published reports citing CBO estimates…timing matters, too. With 2026 rates already set and consumers starting to learn of premium increases, delays in extending the PTC enhancements beyond 2025 have already led to cost increases and coverage losses that cannot be reversed.

These cost increases come on top of the largest Medicaid cut in history, which Congressman Bresnahan voted for after promising his constituents that he would not cut Medicaid.

The Bresnahan Soaring Costs campaign has held protests and events holding Congressman Bresnahan accountable for his refusal to extend health care tax credits. And we intend to continue.

Below is a timeline of every time Congressman Bresnahan refused to extend health care tax credits, pushing us toward the health care cost crisis we’re in:

July 4 – Despite warnings from experts and advocates, Congressman Bresnahan & Congressional Republicans refuse to include expiring health care tax credits in the Republican Tax Law and, instead, prioritize expiring tax breaks for the ultra-wealthy.

Pennie: The Impact of H.R. 1 Marketplace Provisions and Expiration of Tax Credits

“H.R. 1 drastically increases costs for low- and middle-income Pennsylvanians in three ways. First, the legislation fails to extend the enhanced premium tax credits (EPTCs) that have made affordable health coverage a reality for many Pennsylvanians.”

“…the ‘One Big Beautiful Bill Act’ is missing something health care advocates hoped to see: an extension of the insurance premium tax credits under the enhanced Affordable Care Act that are set to expire at the end of the year. The credits’ absence is notable as the bill includes other proposed changes to the ACA marketplace, experts say.”

KFF Health News: Four Ways Trump’s ‘One Big Beautiful Bill’ Would Undermine Access to Obamacare

“Major changes could be in store for the more than 24 million people with health coverage under the Affordable Care Act, including how and when they can enroll, the paperwork required, and, crucially, the premiums they pay. A driver behind these changes is the…The House-passed One Big Beautiful Bill Act, which runs more than 1,000 pages, would create paperwork requirements that could delay access to tax credits for some enrollees, potentially raising the cost of their insurance…Enhanced tax credits created during the pandemic expire at the end of the year. The House bill doesn’t extend them. Those more generous payments are credited with helping double ACA enrollment since 2020.”

October 1 – Congressman Bresnahan & Congressional Republicans shut down the government with their refusal to extend the tax credits by the October 1 deadline when insurance companies locked in higher premiums.

Georgetown Center on Health Insurance Reforms:

“On September 23, CMS announced that insurers would have until October 1 to make any changes to premium rates, and until October 2 to sign their contracts with the federal Marketplace. They have now reached a ‘pencils down’ moment…In other words, CBO believes that a premium increase of about 5 percent is already locked in. Any such late rate revisions would also impose costs on issuers, Marketplaces, and state regulators that would be passed along to consumers and taxpayers.”

“An assumed enactment after September 30, 2025, would affect CBO’s estimates in two ways. First, in CBO’s estimates, the likelihood that gross premiums for 2026 would be adjusted downward would fall to zero after the start of open enrollment. November 1, 2025, is the start of the enrollment period for the 2026 plan year in most marketplaces. Second, the estimates would reflect a smaller likelihood that enrollees will see net premiums that incorporate the expanded credit structure at the time they select their marketplace plan (the net premium is the amount of the premium after accounting for the tax credit). CBO estimates that an enactment date later than September 30 would result in lower costs to the federal government and smaller increases in 2026 enrollment than those presented here.”

National Association of Insurance Commissioners:

“NAIC has voiced its strong support for continuation of the enhanced premium tax credits for Marketplace coverage. The enhanced credits expire at the end of this year, but health insurance premiums for 2026 must be finalized much sooner. Health insurers have already filed their initial rates for 2026, and state regulators are poised to give them final approval in the coming weeks. We must complete this action soon in order to make plans available for the annual Open Enrollment Period that begins on November 1.”

November 1 – Congressman Bresnahan & Congressional Republicans refuse to extend coverage by the start of Open Enrollment, leading consumers to begin dropping coverage to avoid price hikes.

Georgetown Center on Health Insurance Reforms:

“On November 1, the open enrollment period opens nationwide (and October 15 in Idaho). At that point, both new applicants trying to enroll and current enrollees updating their applications and shopping will see higher net premiums, deterring many from enrolling.”

December 15 – Congressman Bresnahan & Congressional Republicans refuse to extend tax credits by the day when millions of Americans become auto-enrolled in health insurance plans they may no longer be able to afford.

Georgetown Center on Health Insurance Reforms:

“In December, all enrollees–including those auto-reenrolled–will receive their January 2026 bills showing their net premium for 2026. For auto-reenrollees in the federal Marketplace who don’t go in to shop, this will generally be the first time they see the higher premium, resulting in an additional round of disenrollment… In addition, December 15 is the last day to enroll for January 1 coverage in the federal Marketplace.”

December 31 – The ACA Enhanced Premium Tax Credits expire.

KFF:

“Expiration of the enhanced premium tax credits is estimated to more than double what subsidized enrollees currently pay annually for premiums—a 114% increase from an average of $888 in 2025 to $1,904 in 2026.”

“Only 73% of current enrollees are eligible for premium tax credits in 2026, compared to 90% historically, due to EPTC expiration. Without EPTCs, monthly premiums for Pennie enrollees have increased by 102% on average.”

January 31 – Congressman Bresnahan & Congressional Republicans fail to extend tax credits by the end of Open Enrollment in Pennsylvania, locking in high costs and causing many to lose coverage.

The Hospital & Health Association of Pennsylvania:

“While the individual marketplace for coverage on the federal marketplace for healthcare.gov ended on January 15, consumers in Pennsylvania have a few extra days to pick plans.

[…]

“Here’s what you need to know:

- Higher costs: Negotiations to extend enhanced premium tax credits have stalled in Congress, leading to higher costs for insurance coverage on Pennie and other individual marketplace.

- In Pennsylvania: Costs have risen by 102 percent for Pennie enrollees in 2026 due to the expiration of the enhanced premium tax credits.

- Over 70,000 Pennsylvanians have dropped coverage as a result of the higher prices—nearly 1,000 a day for most of open enrollment.”

Congressman Rob Bresnahan owns the health care crisis, forcing millions of Americans to lose coverage and millions more to pay hundreds and thousands of dollars more for the care they need.

The Congressman can run but he can’t hide from his record. He increased health care costs for millions of Americans while getting rich(er) buying and selling stock in Congress. He must right this wrong by listening to his constituents, fighting for lower costs, and putting working families first. for millions of Americans while getting rich(er) buying and selling stock in Congress. He must right this wrong by listening to his constituents, fighting for lower costs, and putting working families first.